Financial Markets

Market conditions fluctuated considerably during the recently completed quarter. Stocks rallied broadly until mid-August only to give it all back, and then some, in the second half of the period. Equities fell as investors anticipated economic headwinds given renewed inflation concerns and heightened resolve by the Federal Reserve to fight it. In total, the S&P 500 Index had a -4.9% return for the quarter, with the year-to-date decline now amounting to 23.9%.

The primary international indices fared worse, posting double digit losses for the quarter with year-to-date returns approaching -30%. Beyond their own bouts with post-pandemic related inflation, many international economies are confronting unique challenges. Europe is grappling with deteriorating relations with Russia, which is a major supplier of oil and gas for the continent but is cutting supplies in retaliation for Europe’s support of Ukraine. China continues to invoke periodic lockdowns due to its “zero-COVID” policy, thereby reducing economic activity as well as manufacturing output. Emerging markets are suffering from weaker currencies as investors pull out of assets in those countries in favor of safer, higher yielding assets in the US and other developed markets.

Rather than acting as a diversifying asset and offset to declining equity prices, bonds fell right along with stocks. The Federal Reserve has significantly increased the overnight lending rate between banks and signaled that more rises are likely in the coming months. This caused interest rates on shorter-maturity bonds like the 3-month Treasury bill to rise sharply. Longer-term bond yields also increased substantially; the yield on the 10-year Treasury bond moved from 2.98% to 3.83% during the quarter. Credit spreads also continued to widen—a reflection of investors’ fading appetite for risk. All told, the Bloomberg US Aggregate Bond Index lost an additional 4.8% during the quarter, with year-to-date losses for the typically staid asset class now 14.6%.

Investment Perspectives

Economic conditions continued to evolve during the third quarter. Recently released data showed that US GDP had contracted for the first two quarters of the year, pointing to a “technical recession.” However, despite flagging GDP readings, the resilient labor market and consumer spending have buoyed the economy and given the National Bureau of Economic Research (NBER) reason to hold off on officially deeming the economy in recession thus far.

The Federal Reserve, as it emphasized last autumn, has remained data driven in its policy decisions. Such an explicit stance has heightened market volatility as each relevant economic data release is scrutinized closely for implications of future interest rate policy. Indeed, recent data has pushed the Federal Reserve to tighten monetary policy at a pace faster than expected and increased the probability of recession.

All Eyes on Inflation

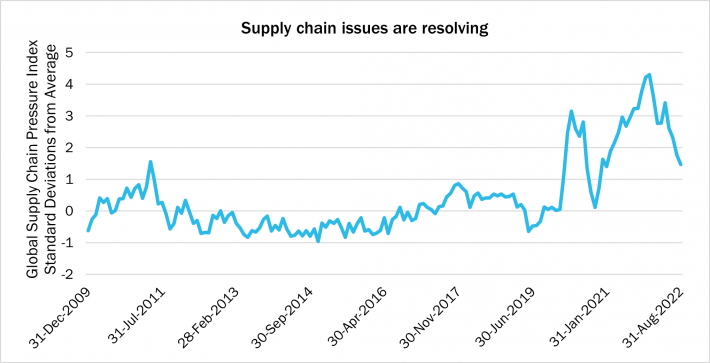

Inflation has remained higher and more persistent than economists and investors originally anticipated, but its causes have evolved. For example, supply-related shocks have begun to subside. Supply chains, roiled by numerous pandemic-related disruptions, labor shortages, and other issues, are recovering. The New York Fed tracks and integrates relevant supply chain data into a Global Supply Chain Pressure Index. Though the Index remains at historically elevated levels, it shows considerable easing from the peak of the strains in late 2021. Such progress may serve to increase availability—and limit cost pressures—of intermediate goods used in manufacturing, as well as final goods purchased by consumers.

Source: Federal Reserve Bank of New York

Source: Federal Reserve Bank of Atlanta

Activity in Washington

The Inflation Reduction Act became law in August. Despite its name and projections of lowering the deficit, we do not expect the law to contribute materially to lowering inflation in the short-term. Nor do we expect it to provide a jolt to the economy. However, the energy and healthcare related spending could have significant long-term impacts. The law provides both producers and consumers with increased incentives—and greater certainty regarding their availability—for alternative energy investments. It also seeks to provide a governor on rising healthcare costs—particularly those related to prescription drugs. Accordingly, the legislation may reduce longer term inflationary pressures in those realms.

The corporate tax changes to pay for these measures are noteworthy as well. Though permitted exceptions and adjustments abound, large corporations will now face a 15% minimum tax. This provision follows efforts in recent years to keep corporations in the domestic tax base and close loopholes. The excise tax on stock buybacks is a new endeavor. At 1%, we do not expect the tax will significantly alter strategies for returning cash to shareholders. However, with such a tax now established, a future increase, should one occur, could be more impactful in corporate capital allocation decision-making.

We are once again heading into election season. We will refrain from prognosticating and only note that polls point to a “split” government with Republicans at least gaining control of the House. Such a result will likely slow the gears of legislation.

Outlook and Positioning

The old adage “don’t fight the Fed” is apt in the current environment. Indeed, our expectation aligns with the consensus in that the Federal Reserve is resolute in its efforts to tamp down on inflation and is willing to risk an economic downturn to accomplish that goal. We also expect investors to continue to react sharply to new data, thereby extending the recent spate of volatility in financial markets.

Beyond the Fed’s actions, other risks to the global economy are evident as well. Among them are China’s COVID policy—which has the potential of impeding supply chain recoveries—as well as the country’s stance toward Taiwan, which risks geopolitical turmoil on a global scale. Additionally, economic conditions in Europe are deteriorating. Besides representing a significant portion of the global economy, Europe is also an important market for many US companies. Among other concerns, high natural gas prices are stoking inflation and softening the economy, with potential for further degradation in the winter heating months.

Though a Fed-induced slowdown will continue to have wide-ranging impacts, certain pockets of the domestic economy have remained resilient. Most prominently, these include consumer spending—a reflection of both the exceptionally strong labor market and still robust consumer savings—as well as corporate profits. Though there has been some deceleration in the pace of corporate earnings growth, most businesses have thus far weathered the storm of inflation and rising interest rates remarkably well. This is particularly true of the types of companies we favor: those with sustainable business models and the pricing power to pass along rising input costs to protect profit margins. We do not foresee permanent impairment of the long-term earnings power of such companies, but rather have simply seen a change in the valuation of their shares. As earnings growth ultimately drives stock prices over the long-term, the now lower valuation of quality companies underlies our continued preference for stocks in multi-asset portfolios. To be sure, the recent rise in interest rates has made yields on safe fixed income instruments more appreciable, and thus provide more attractive expected returns for bonds serving as a portfolio ballast and/or as a repository for near-term cash needs.